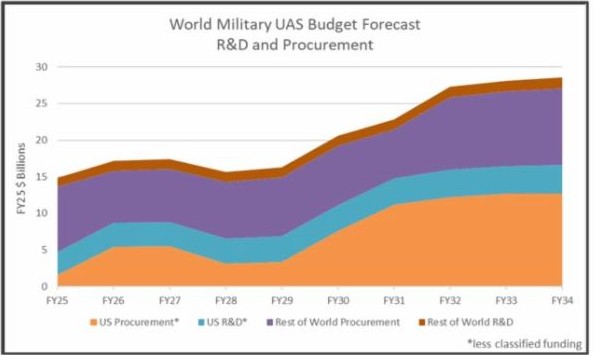

In terms of worldwide military budgets, the unmanned aircraft systems (UAS) segment continues to see growth, although annual growth has moderated when compared to a decade ago. The unclassified sector will continue to increase over the next decade, by about 91.9%, almost doubling, from current annual spending on RDT&E and procurement of about $14.9 billion in FY25 to about $28.6 billion in FY34 (a CAGR of 7.5%). If operations and maintenance expenditures were to be added, these totals would be greater.

In terms of worldwide military budgets, the unmanned aircraft systems (UAS) segment continues to see growth, although annual growth has moderated when compared to a decade ago. The unclassified sector will continue to increase over the next decade, by about 91.9%, almost doubling, from current annual spending on RDT&E and procurement of about $14.9 billion in FY25 to about $28.6 billion in FY34 (a CAGR of 7.5%). If operations and maintenance expenditures were to be added, these totals would be greater.

3900 University Drive, Suite 220

Fairfax, Virginia 22030

Send Email Message

Toll Free: (888) 994-TEAL (8325)

Tel: (703) 385-1992

Fax: (703) 691-9591

© 1988 - 2024 Teal Group Corporation

3900 University Drive, Suite 220

Fairfax, Virginia 22030

Send Email Message

Toll Free: (888) 994-TEAL (8325)

Tel: (703) 385-1992

Fax: (703) 691-9591