Special Offers!

For a limited time, receive additional savings on multi-title subscriptions:

- Any two or more newly-subscribed titles purchased receive 20% bundle discount (excludes the Military Electronics bundles, which are already permanently discounted)

- Add an additional title to your renewal and receive a 20% discount on the new title!

- Realize a progressive discount the more titles purchased

Promotional offers end 31 December 2024. Offers not available through the website.

Contact Sales directly for promotional orders:

Jim Head, Sales Director

JHead@TealGroup.com

tel 203 770 9522

25 September 2024

Aircraft deliveries trimmed again

While there has been plenty in the Commercial Aviation space to talk about (see below), we want to start the missive with our latest feature, our Commercial Aircraft Fleet Development Forecast. Astute readers may already have seen glimpses of these in our annually updated commercial aircraft reports that have been issued since June, and which we will add to the rest of the reports as they come up for updating over the course of the next 11 months.

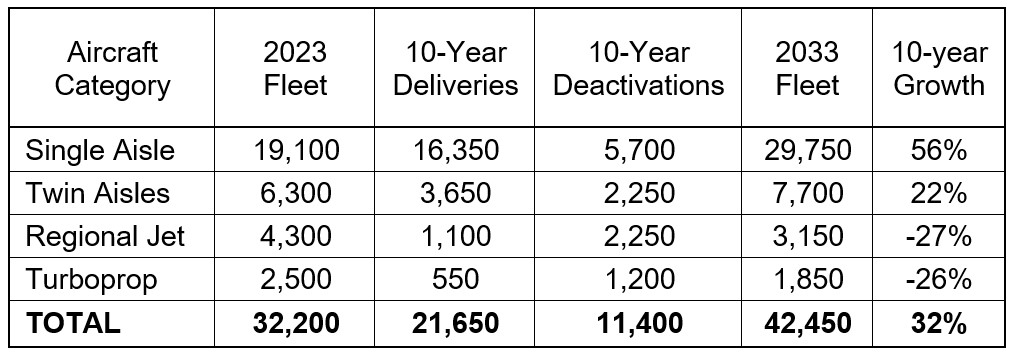

Our analysis begins with our internal database of historic deliveries combined with a retirement model that we have developed internally based on industry trends. We verify the active fleet as of the end of the most recently completed calendar year using open-source references, and then add in our forecast of deliveries and subtract out expected retirements based on the model. Our analysis covers over 60 different aircraft types and significant variants, for aircraft both in production and out of production, from 30-seat turboprops to 550-seat jets and includes both passenger and cargo aircraft.

The table below shows the results of this analysis. To summarize, we estimate that in 2023 there were a total of approximately 32,200 active commercial aircraft. Over the next 10 years, we are forecasting deliveries of nearly 20,650 aircraft and over the same period, and, based on our model, we are forecasting deactivations (retirements plus accidents and old aircraft just sitting around) of nearly 11,400 aircraft, leaving a total fleet in 2033 of 42,450. The table below shows the breakout by category.

While the total fleet grows by almost 32%, single Aisles account for more than all the growth, going from just under 60% of the fleet in 2023 to over 70% in 2033. The shares of the other categories all go down: Twin Aisles go from nearly 20% to 18%; regional jets from 13.5% to 7.5%; and turboprops from almost eight percent to 4.5%.

As for the current situation in the aviation business, seven months into 2024 it’s not looking as rosy as we thought as the year started out. While much of the blame is being heaped on the supply chain - specifically engines, seats and heat exchangers - the biggest culprit is Boeing’s self-induced slowdown of 737MAX deliveries following the Alaska Airlines incident in January while they sorted out their production issues. We once thought there would be as many as 575 MAXs delivered in 2024, but we’ve slashed that to around 360. In dollar terms, that’s nearly a $12 billion shortfall, which explains why Boeing seems to be burning through $1 billion a month. We’ve also trimmed the 787-delivery forecast following all the unhelpful news that that program seems to be generating recently. Right now, we aren’t forecasting a change in the 10-year output of both programs, mostly because of the robust backlogs for both. This implies that future ramp-ups will need to be steeper and the delivery peak higher than we initially thought. But the longer these delays go on, one must wonder whether it won’t take a toll on demand, and thus longer-term output.

For its part, Airbus has guided that it will only deliver 770 aircraft this year, after guiding to 800 early in the year. Coincidentally, our Airbus forecast at the beginning of the year was right around the 770 figure, so we haven’t adjusted our 2024 Airbus delivery forecast.

For its part, Airbus has guided that it will only deliver 770 aircraft this year, after guiding to 800 early in the year. Coincidentally, our Airbus forecast at the beginning of the year was right around the 770 figure, so we haven’t adjusted our 2024 Airbus delivery forecast.

In the business jet space, deliveries (dollar wise) are being supercharged by G700s, which the FAA finally certified in March this year. Bombardier seems to be doing well, too, while others are exhibiting mixed results, mostly owing to supply chain challenges, but remain hopeful for the remainder of the year. So far, we haven’t adjusted our business aircraft delivery forecasts for 2024, but we’ll be watching the space for some adjustments. That said, we’ve noticed a tendency for business aircraft deliveries to spike in the fourth quarter.

While the supply chain continues to challenge, the other long pole, the regulatory side, seems to be providing some level of encouragement. In mid-July the 777X got its Type Inspection Authorization from the FAA. Boeing seems to think that it can still deliver 777Xs in 2025, but customers seem to be managing expectations for a 2026 EIS. And both might be true; one could definitely see a scenario where the initial 777Xs could be delivered in, say, December 2025, while operators don’t get around to actually carrying passengers until well into 2026.

Further encouragement came from EASA later in the month when it certified the A321neoXLR. The certification was only for the 97k-tonne version instead of the 101k-tonne version Airbus is ultimately touting for it to achieve the full 4,700 nm range. It was interesting to note that Airbus seemed to intimate that some customers’ A321neoXLRs might be coming in with higher OEWs – due, we gather, to heavier than expected premium seats – further necessitating the higher weights. This development hasn’t changed our A320neo forecasts as we fully expected the aircraft to be certificated and delivered. While the certification came later than Airbus hoped, we don’t think the XLR is going to move the needle on A320neo deliveries noticeably in the near term.

Finally, we would be remiss if we didn’t mention the Farnborough International Airshow. Order-wise it didn’t really register much of an impact. The only 100+ firm new orders announced (the only ones that really matter), paled in comparison to other more recent air shows (Dubai, Paris). Of note, however, was the relatively heavy twin-aisle contribution to the mix. This reflects the full order books for single-aisles and improving fortunes of Asian carriers.

WMCAB subscribers can view the detail by logging into their Teal Group account and clicking on the Commercial Aircraft link in our spreadsheets section. To inquire about subscribing, visit our website.

- Posted in: News Briefs

About the Author

Bruce McClelland

Bruce is a Senior Contributing Analyst at Teal Group. He is responsible for editing the World Power Systems Briefing – Industrial and Marine Gas Turbines, and the Defense and Aerospace Agencies Briefing, as well as providing contributing analysis for Civil Aviation consulting projects at Teal.

3900 University Drive, Suite 220

Fairfax, Virginia 22030

Send Email Message

Toll Free: (888) 994-TEAL (8325)

Tel: (703) 385-1992

Fax: (703) 691-9591