16 February 2022

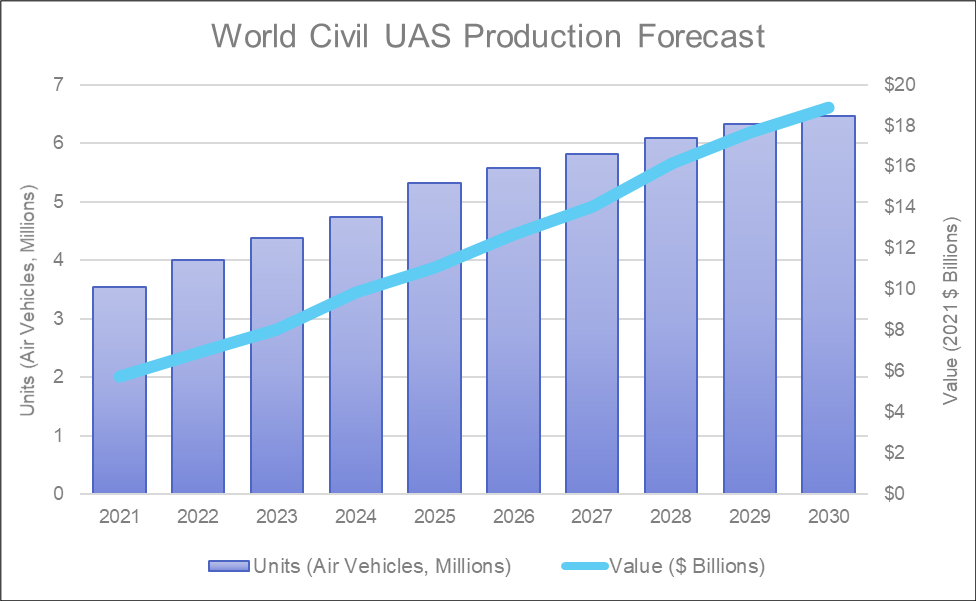

Civil UAS Market Opportunities Crystallize

The battle for the consumer drone manufacturing market is over, with China’s DJI Innovations dominating the market. Even DJI has tacitly acknowledged the consumer market has become mature, as evidenced by its move into higher level, more sophisticated systems.

The battle for the consumer drone manufacturing market is over, with China’s DJI Innovations dominating the market. Even DJI has tacitly acknowledged the consumer market has become mature, as evidenced by its move into higher level, more sophisticated systems.

On the other hand, the markets in commercial drone manufacturing, services and analysis are still up for grabs. This middle market, ranging from prosumer units to lower-end MALE systems, stands to enjoy the most significant growth in our forecast period, particularly as regulations evolve to permit their use in more countries and roles. US, European, and Asian companies are battling worldwide for positions in systems and services to address this market. While this attracts numerous new entrants, particularly to niche markets, the drive for scale has begun as mergers and acquisitions nationally and across borders accelerate.

As the worldwide industry develops, national and regional advantages are emerging.

The United States is the clear leader in analytics and the development of service offerings. Tremendous interest by technology leaders such as Intel Corp., Amazon, Facebook, Google, Sony, Verizon, Mitsubishi, General Electric Co., Microsoft, Apple, and Samsung is adding to the speed of development by providing financing and an infusion of new technology and talent. Major technology firms such as Intel, Microsoft and Qualcomm are working to apply their technologies to making drones effective work tools.

An infusion of venture capital is creating an industry of startups in both manufacturing and the services that will be critical to development of the commercial market. Two-thirds of the venture capital money worldwide is going into the US drone industry.

In many cases, US companies’ analytical advantage in fields like infrastructure inspection or soil surveys has made them platform-agnostic. They can work with Chinese UAS as easily as American-made drones, and although numbers of mid-tier US startups like Harris Aerial are emerging to bring capability to niche markets, it’s not yet clear that the United States can or will be able to claim an advantage in hardware production.

China’s clear advantage is in manufacturing. The nation is seeking to expand from dominance in consumer UAS manufacturing to leadership in commercial UAS. Government and industry are working together to build their country’s market presence in agricultural and delivery drones, two of the largest potential sectors in the future. Yet other Chinese companies are working to move into drone production for specialized inspection areas such as powerlines and wind turbines. This upward evolution will move some significant Chinese companies from markets they currently dominate into ones where other companies have established leading positions.

Despite vocal support from the Japanese government, Japan is falling behind China. Japan emerged as an early leader in civil UAS development thanks to an unmanned agricultural spraying industry that dates back three decades. Japan’s most promising potential areas to play a role in the worldwide UAS industry come in agricultural spraying, smart construction work, and services. In each of those cases, Japan’s lack of manpower is driving national adoption of unmanned systems.

Europe has already ceded its early lead in drone market development to the United States and China. Europe is working to avoid being left behind by enacting standardized airspace rules that will create a single market. The European Aviation Safety Agency (EASA) led the harmonization of European national regulations by establishing rules for small UAS across the European Union and issued its guidelines for verifying UAS designs in April 2021.

European UAS firms are falling behind in this flurry of activity. They lack the strong venture capital funding enjoyed by US firms and the large, unified domestic drone market of China. As a result, some European drone firms have either moved their headquarters or significant operations to the United States. The new EASA rules should help remedy this situation.

The worldwide drone market’s evolution is clear from venture capital trends. Increasingly venture capital funding is shifting from hardware to software and services that will make existing drones more useful. Funding is being used to develop the business tools that are needed to quickly allow industry to develop scale, such as national networks of service providers and improved analytics to make UAS easier to use and more proscriptive. VC funds are also going to the companies that will lay the foundations for access to airspace such as detect and avoid technology and unmanned traffic management.

- Posted in: News Briefs

About the Author

J.J. Gertler

A veteran of aerospace program analysis since 1984, Jeremiah Gertler joined Teal Group in 2021, providing insight to private clients worldwide. He is the current editor of Teal’s annual World Civil UAS Market Profile and Forecast.

3900 University Drive, Suite 220

Fairfax, Virginia 22030

Send Email Message

Toll Free: (888) 994-TEAL (8325)

Tel: (703) 385-1992

Fax: (703) 691-9591